About shega

Team

Careers at Shega

Contact

SEM

Jobs

Opportunties

Games

Tools

No post found with this title. It might have been removed or renamed. Please go back or use the search to find something similar.

What the IMF Fifth Review Actually Says About Ethiopia's Reform Trajectory

20 July 2026

Liberalization of Ethiopia’s Banking Sector: Foreign Entry, Competition, and Digital Finance

17 July 2026

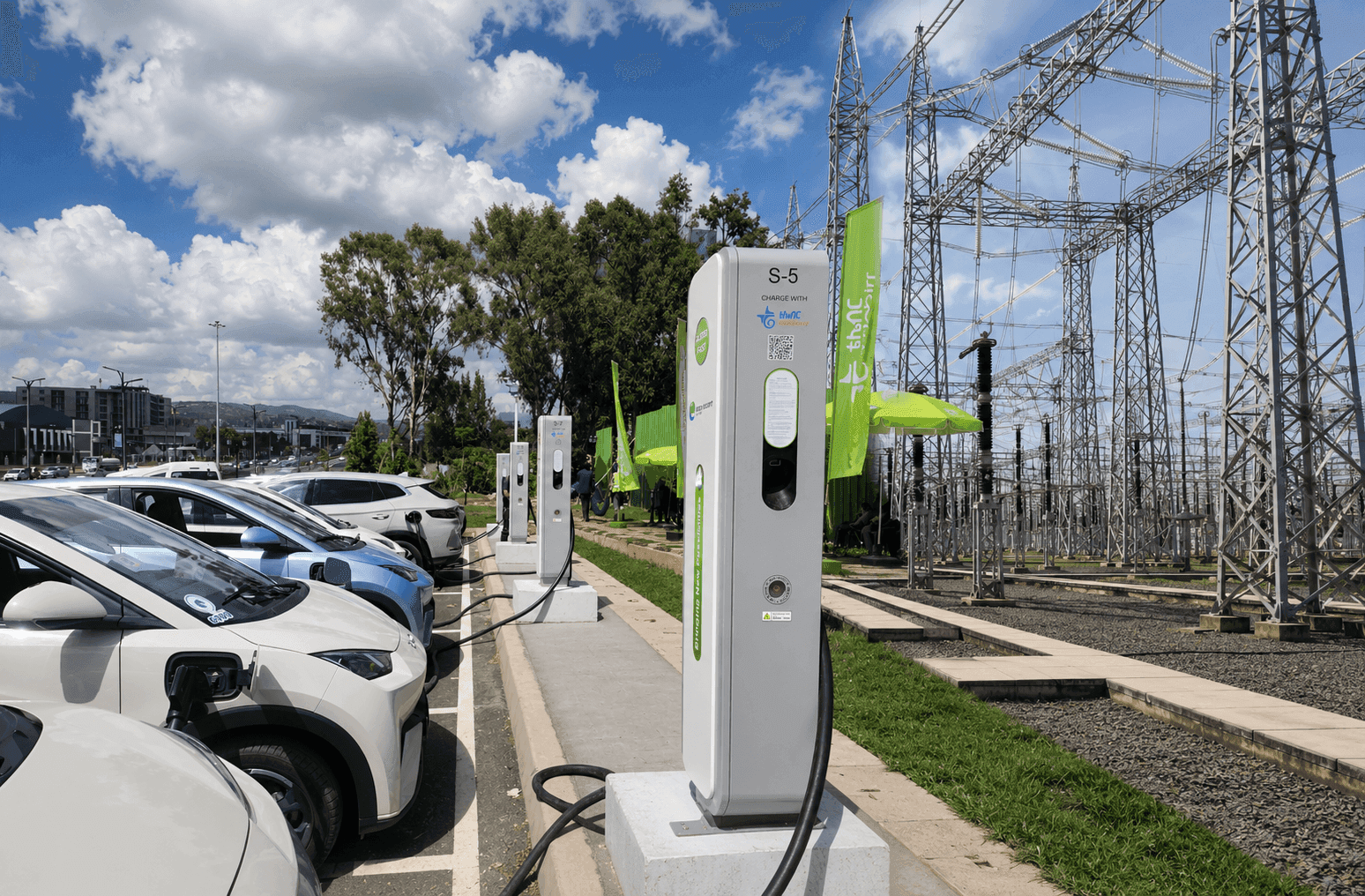

Ethiopia's Electric Leap and the Road It Hasn't Built

16 July 2026

Addis Moves to Stabilize Construction Inputs with New Mineral Licensing

14 July 2026

Punctual, Not Audacious

13 July 2026

Too Big to Regulate? CBE Says It Accounts for 70% of Digital Transactions

10 July 2026

Ethiopian HealthTech Founder Wins Bayer Foundation Women Entrepreneurs Award 2026

07 July 2026

Ethiopia's Eurobond Restructuring is a Second Act, Not a Finale

06 July 2026